Tier-1 companies in coal tar manufacturing represent 60-70% share of the total market revenue. With massive coal tar distillation capacities across the globe, these players in coal tar pitch landscape maintain their focus on both, standard grade and special grade coal tar pitch (CTP) production.

Tier 2 players have a strong presence over restricted regions, whereas that of Tier 3 competitors is limited to regional sales. Standard grade coal tar pitch is the key focus area for the latter two, according to Future Market Insight’s study on the global coal tar pitch landscape.

“Production facility expansion, strategic acquisitions, and CTP product innovation will remain the key developmental strategies trending among leading players,” says a senior research analyst at FMI. The analyst adds further, “Massive Aluminum demand from automotive and transportation sectors has been pushing the Aluminum production levels 4-5% (yearly) since the recent past. Growing demand for lightweight vehicles is among the most impactful factors driving the consumption of Aluminum, subsequently contributing to sales of coal tar pitch”.

Long-term Contractual Partnerships & Backward Integrated Supply Rule Strategic Minds of Coal Tar Pitch Manufacturers

While manufacturers of coal tar pitch are preferring long-term supply contracts with leading coal tar manufacturers, FMI has also identified these players entering strategic partnerships with steel manufacturers, where coal tar is often the byproduct of coke processing ovens. A few other activities that make this landscape dynamic include long-term contracts between manufacturers of coal tar pitch and those of primary aluminum and graphite electrode, with a sole objective to sustain the coal tar pitch supply to end markets.

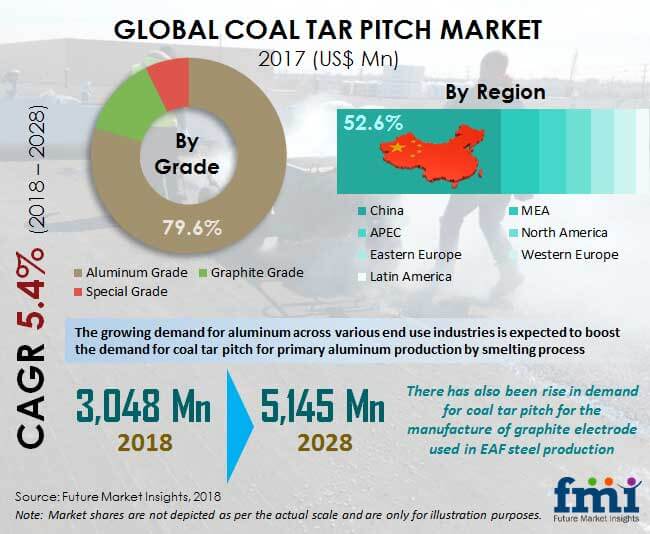

Aluminum Grade CTP Holds a Winning Revenue Share in Coal Tar Pitch Market

Application-wise, around 80% revenue share belongs to the aluminum electrode, according to the study. As coal tar pitch is increasingly being consumed by aluminum smelters lowing to higher sustainability and economic feasibility, the mushrooming Aluminum production is constantly driving the growth of coal tar pitch landscape. In 2019, the revenue of Aluminum grade coal tar pitch is pegged for over 5% Y-o-Y growth. Besides, Graphite electrode is also slated for promising performance and the application base of coal tar pitch as a chemical intermediate in carbon black manufacturing is visibly growing.

Development of Specialized ‘Zero QI Impregnating’ Coal Tar Pitch Expands Applicability

A specialized ‘impregnating’ pitch obtained by processing coal tar at a high temperature is widely used in the Graphite industry during the electrode manufacturing process. The resultant technological advancements in the life of electrodes pushes CTP applications in roofing, coating, electrode, refractory, and others.

For More Details, Ask Analyst @ https://www.futuremarketinsights.com/ask-question/rep-gb-7186

China Commands over Global Coal Tar Pitch Landscape, India Leads Asia Pacific’s CTP Scenario

China, India, Russia, and Western Europe have a significant aluminum production base, whereas MEA is demonstrating promising growth in coal tar pitch landscape in recent years. North America, however, is observing passive growth over the recent past, post decline in the aluminum production levels.

According to the FMI’s report, China is the global leader in coal tar pitch ecosystem owing to significant Aluminum production and thriving production levels of Graphite electrode. China is projected for a 6% year on year revenue growth by this year’s end, reflecting ample growth opportunities for coal tar pitch manufacturers.

On the other side, APAC’s market for coal tar pitch is witnessing growth concentration in India that has been attributed to an impressive rate of Aluminum production in the country.